Ethereum Is Not Decentralized

Recently a friend of mine was telling me his thesis about how he thinks Ethereum will succeed even if it doesn’t scale properly.

A network like ETH provides a lot more value than just being a scalable protocol. It stores and protects hundreds of billions (soon trillions) in value and does so without the need for traditional banks. That alone is incredibly valuable.

Some say ETH is becoming silver to BTC’s gold, but I think that is even downplaying the network effects and liquidity building on ETH. Just watch.

I’m a Bitcoiner and he’s a VC/trader/wealth manager who has long believed in Bitcoin (holds majority of his networth in Bitcoin) but also makes alpha over Bitcoin in bull markets by trading & investing in altcoins like ETH and others.

This line of thinking is actually what Bitcoiners preached from 2016–now. During the scaling debate, big blockers took the argument that unless Bitcoin can scale to Visa level & serve the payments usecase, Bitcoin will fail.

They wanted Method of Exchange before Store of Value. Small block bitcoiners argued that Bitcoin could succeed as a global store of value competitor to gold in the trillions of marketcap without ever serving the method of exchange use case.

Small block Bitcoiners wanted to see scaling happen on sidechains and second layers to keep the base layer as decentralized as possible to allow anyone to run a node with consumer grade hardware.

As more & more transactions go onto the base layer, the hardware & bandwidth requirements to run a node go up until average users are priced out and only corporations & datacenters are able to run nodes.

At that point, the decentralized properties of the network are in jeopardy, neutering the censorship-resistant properties of the system, which then allows for easy government capture.

The developers & node operating users of Bitcoin won the scaling war in 2017, and so far, small block Bitcoiners have been proven right. The network is starting to scale out in second layers & side chains like Lightning Network & Liquid, while serving the store of value use case & retaining the critical feature of decentralization on the base layer.

When it comes to Ethereum, it is meant to be a way for anyone to build “unstoppable code” to run decentralized applications cheaply & trustlessly on a “world computer.”

Ethereum has already failed the immutability test once when the DAO exploit happened and Vitalik decided to forego decentralization & roll back the chain & fix it.

Ethereum has also failed the scalability test in 2017 when the ICO craze & a lone dApp CryptoKitties broke the usability of the chain.

Bitcoiners said it was unscalable to put everything on the base layer, and we were right. Ethereum fees right now are higher than Bitcoin fees — and for some complicated DeFi or NFT transactions, the ETH fees are 10X higher than Bitcoin fees.

https://www.youtube.com/watch?v=unMnAVAGIp0

After the bear market of 2018/2019, DeFi emerged as the latest use case that Ethereum investors & devs got excited about.

Many of us are critical of the ever changing narratives of Ethereum, from “Ethereum is a world computer & ETH is smart contract fuel” to “Ethereum is a settlement layer for decentralized finance and ETH is ultrasound money”

I don’t hear the old refrain “unstoppable code” anymore since the DAO rollback, and barely anyone talks about dapps or ICOs … that’s been replaced with talk of DAOs and NFTs.

To give credit where credit is due, during the Ethereum ICO, Vitalik had written about the idea of the lego blocks of finance. You can go back into the marketing materials of the ETH ICO and see that decentralized finance, and many other use cases, were discussed back then.

In 2018 the SEC started to take actions against the teams who did ICOs on Ethereum, which gave clear precedent that ICO coins were illegal securities. The SEC issued a statement saying the DAO was an illegal security, and so was ETH at the time of the crowdsale.

They didn’t make an official statement about ETH currently, but a senior SEC official made a personal statement, not speaking on behalf of the SEC, that ETH was currently not a security.

The story of whether or not ETH is a security is actually not resolved yet, more definitive clarity should come after the resolution of the ongoing SEC lawsuit against Rippple/XRP. As far as I understand it, as part of their defence, the XRP lawyers have asked the SEC to provide documentation on whether or not ETH is a security, and the criteria describing how they came to that decision.

Utility tokens got absolutely routed in the ICO bubble pop, and during the Crypto bear market, it looked like the fat protocol thesis was mostly disproven.

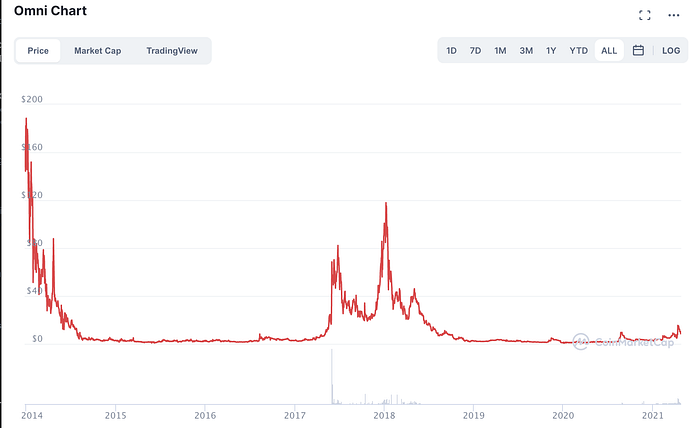

It was about this time that USDT was moving from the Omnilayer on Bitcoin to Ethereum (and then later they moved onto Tron & Blockstream’s Liquid Network Bitcoin Sidechain.)

The free market was making a statement that value was going to continue to accrue to the companies building technology, not the utility coins of crypto networks.

The idea of MV=PQ was being disproven as well.

Ethereum proponents pointed to the transaction volume of USDT stablecoins being settled on Ethereum citing MV=PQ logic.

BCH & other proponents of blockchains with a lot of transactions would always use this network transfer / settlement value as a reason to say that value was going to accrue to the base layer token of the network.

However, fundamentally if that were the case, then the OMNI token would have been valued at a much higher marketcap than it was.

USDT was being settled through OMNI on Bitcoin for years, and Bitcoiners never used the volume of tokens like USDT to value the BTC token.

The value of OMNI token was not rising based on the MV=PQ thesis which posits that the network’s token should accrue value based on the increase of settled transaction volume & rise in marketcap of USDT.

It was only rising based on the fomonomics of the 2017 crypto bubble … everything went up.

BTC on the other hand *is* money.

Only on a sound base layer of long term credible scarcity & decentralized censorship-resistance do the other network effects start to accrue as modifiers & multipliers to the valuation of the BTC token.

I find it telling that only the transaction volume of BTC itself was/is counted by Bitcoin analysts. Altcoins need to compete with Bitcoin’s Lindy Effect & superior monetary properties, so they need to invent new valuation metrics and count whatever makes their narrative sound different … then in the end, all Altcoins including ETH are competing with BTC as a monetary Store of Value.

By 2020, rationality was back into the market. Price of all coins against Bitcoin was the ultimate signal that most of Crypto valuations were just bad ideas & weak logic.

The previous Ethereum narratives of ICOs disrupting Venture Capital & “tokenize the world” were embarrassing remnants of a nonsensical bubble.

DeFi was built out, but teams were running out of money. Zcash, Cardano & Consensys abused the covid PPP loan program. Consensys had to lay off staff & they were close to being acquired by acquired by JP Morgan…

Ethereum’s security was in jeopardy as Consensys had to invest $20 million into Ethereum Mining to secure the blockchain from a relatively cheap 51% attack vector leading up to the final time period between PoW & the switch to PoS.

DeFi was only being used by the surviving crypto funds, ETH developers & Silicon Valley VCs like A16Z & Coinbase Ventures who were propping up projects like Maker/DAI.

Uniswap was showing that there was an interesting use case for decentralized exchange, but it had barely any usage because the UX of DeFi was terrible compared to Centralized Crypto Finance like binance, blockfi, coinbase, etc.

Occasionally there would be a smart contract exploit or a a flash loan exploit in which some quant was able to take advantage of the “code is law” meme and exploit a protocol. Often, teams would use their centralized admin keys to fix the problem.

So what happened? How did we go from a state of DeFi where it was only being used by ETH devs & quants to the current state where nearly every crypto trader, crypto VC, crypto fund & crypto influencer has a metamask and is doing some sort of DeFi farming?

Did the regulators decide that doing ICOs was ok? Did they decide that AML & KYC rules no longer apply to crypto?

No, that’s not what happened, but it certainly feels that way. The tides turned for Ethereum & DeFi with the introduction of the ICO 2.0 … Liquidity Mining.

It started with projects like Ampleforth, Curve & Yearn. It was a simple hack on the idea of the ICO.

Instead of taking money for tokens like in a traditional ICO, teams started doing these “liquidity mining” events which allowed them to launch utility coins just like in 2017, including the huge premines for the team, the pre-seed investors & friends of the project … except these liquidity mining programs allowed teams to claim that a “DAO” was issuing the tokens, by deploy smart contracts that issued tokens for depositing money into liquidity pools or using the DeFi apps.

Nobody is really going to be fooled by the argument of hiding behind a Mintr contract…

Combine this with “Generalized Mining” aka ETH whales locking up ETH, USDC & WBTC into the pools to simulate usage, and labeling the ICO issuances as “yield farming” it started attracting other crypto whales to the party.

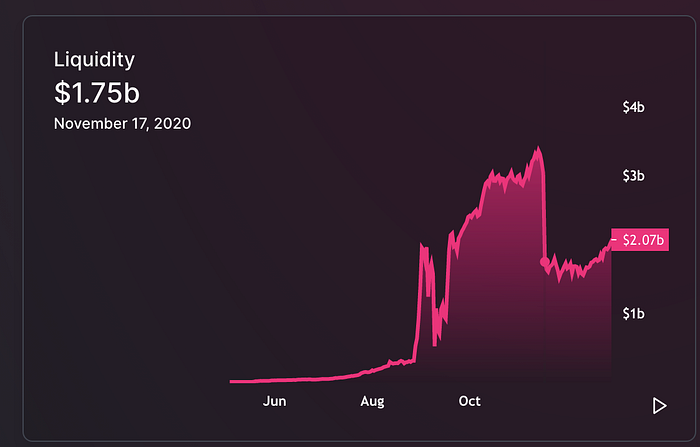

DeFi Summer of 2020 happened which found product market fit for Ethereum once again — the crypto casino.

DeFi summer attracted tens of thousands of crypto traders to start using Uniswap, Balancer, Curve, Yearn etc instead of Bittrex, Binance & Coinbase … millionaires were minted from projects like Synthetix, Link which attracted the crypto twitter elites to the party.

Phase 1 of the NFT craze was also kicked off in DeFi Summer with liquidity mining incentives being applied to NFT platforms like Rarible, where you were encourage to wash trade to earn “governance tokens.”

Whales came to deposit billions of dollars in the liquidity mining events, farming tokens & dumping them. The food ponzi summer of 2020 literally saved Consensys & the many teams building DeFi on Ethereum who had run out of money.

Exploits, hacks & rugpulls went from happening once every month or 2, to once every few days. It was common place to see million dollar exploits & multimillion dollar rugpulls…but since the upside was a 1000% APY, degen crypto traders were ok with the risks.

The problem is that Decentralized Finance was never really decentralized, and back to my friend’s initial point about ETH not needing to scale to be successful … well the truth is that Ethereum is not really securing as much wealth in a decentralized way as he and many others think.

Just like the high APYs, everything about Ethereum is deceptive. It’s clear that the perverse incentives of DeFi & the whale/VC honey pots have worked. The shining lights have distracted investors from looking behind the curtain at the serious risks, instead they just look at things like Network Effects.

The last 12 months have seen massive growth in the “TVL” of Ethereum, which is also deceptive metric since it’s not actually locked, it’s just temporarily deposited to capture ridiculously high APYs.

I believe the enforcement of regulations will show how this is not decentralized pretty soon.

FATF guidelines, treasury guidelines, SEC guidelines & FinCen guidelines will be soon enforced.

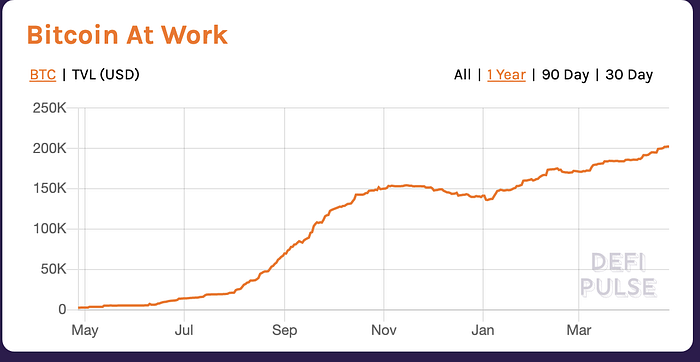

- WBTC is the biggest pool of capital on Ethereum. It’s completely centralized to BitGo. BitGo holds the keys. No real value accrual to ETH in a rational market, no more than the value accrual would be to the mysql database that BitGo uses to keep track of their accounting.

ETH Maximalists will point to this chart and say “Ethereum scales Bitcoin,” using the 200,000 WBTC as a valuation metric while at the same time ignoring the Lindy Effect ceiling of high fees. This is an example of rationalization & flawed MV=PQ logic.

2) Stablecoins are the biggest pool of capital on Ethereum, and it’s also completely centralized. Stablecoins are fundamentally just someone else’s dollars.

WBTC & Stablecoins are all custodial. They can be frozen, and you need to KYC yourself to use them or redeem for non-crypto dollars.

*Caveat is that there’s a small amount of liquidity available on sites like curve, changenow & sideshift where you can try to anonymously go to Bitcoin, but it’s expensive to do that & there’s not a ton of liquidity. For a really high fee, you can also convert your assets to RenBTC or tBTC and get out of Ethereum to Bitcoin in a semi-private way. RenBTC was recently acquired by FTX so there’s also regulatory capture risk there as well.

3) As for the rest of the “soon to be trillions” of dollars on Ethereum, I really think this is my friend just being hyperbolic. I can’t fathom another 20X in this crypto bubble. Currently there’s $50B deposited to ETH, for it to reach 1 Trillion, that would be a significant blowoff top.

A lot of that would be inflated because of the bubble valuation of DeFi coins, governance tokens & ETH, which should all come down in price 90%+ (in Bitcoin terms at least.)

People look at the price and then make up reasons to justify why the price is rising … but the key to surviving a crypto bubble is not becoming a community member.

We are in a market where Ripple is a 50 billion marketcap, Dogecoin is a 35 Billion marketcap, BSV is a 5 Billion marketcap and people are finding random bags of old 2017/2018 altcoins worth 6 and 7 figures. This is not sustainable.

Bitcoin Diamond is up 300% this year. A random pirate coin called ARRR has outperformed Ethereum by magnitudes. Show me your favorite “blue chip coin” that’s up because of fundamental reasons and I’ll show you a random shitcoin that’s up higher because of lulz.

4) Users.

Being generous, theres’s at max 300,000 *people* (average crypto users have multiple wallets to farm airdrops) who have ever interacted with DeFi & NFTs on Ethereum.

To be clear, you can check dappradar, defipulse, etherscan or nansen to se that the user numbers are underhwelming compared to the marketcaps & prices of these coins.

The most valuable DeFi coins on Ethereum have a small amount of active users. Still, with only a small amout of people using DeFi, the fees are so high that it’s driving new users away from Ethereum.

The way that the ETH maxis & VCs talk about this, you’d think there were millions of users. It’s mostly crypto whales and VCs putting their funds at risk to print shitcoins in liquidity mining schemes. It’s not sustainable. The active user count of most of the highest valued Ethereum DeFi protocols are in the thousands.

Remember, the only reason that there’s 50 Billion “locked” in DeFi on Ethereum is because of the perverse incentives of the extremely misleading “APY” numbers of liquidity mining. These are the sort of network effects that folks like Raoul Pal don’t factor in when they come up with a thesis of why DeFi & ETH are good investments.

Metcalfe’s Law isn’t a great metric for a network which is attracting network participants with perverse incentives.

When you are literally paid to borrow money from a DeFi protocol, how can you count that user as the same value of someone like Michael Saylor?

If you’re going to use Metcalfe’s Law for Ethereum, you need a huge negative modifier in your calculations considering the network participants are made up mostly of degenerate short term gamblers and uninformed FOMO investors attracted by the extremely misleading “APY” numbers.

DeFi is a honeypot for unsophisticated network participants. The impact of Metcalfe’s Law for an incentivized network like Ethereum DeFi is not the same as the impact of Metcalfe’s Law for an altruistic network like Bitcoin Lightning Network.

The users are there to gain the benefits of something which is not derived from fundamental free market value-generating activity like lending & borrowing … the thing that is driving the high APY’s which users are depositing their money for is built on a foundation of unsustainable subsidies. It’s ponzinomics.

“Lock up ETH, WBTC & Stablecoins & provide liquidity in the shitcoin:ETH or shitcoin:USDC pool and get more shitcoins”

There will be a reconciliation back to fundamental principles at some point when this bubble pops.

The majority of the volume on the DEXes is driven by this same fake fiat money printing. It’s crypto traders doing yield farming & selling these liquidity mined shitcoins to the liquidity pools.

It’s literally printing money from thin air, and it’s a massive game of chicken. In Nov 2020, DeFi Summer ended when the whales started withdrawing their liquidity from the DeFi farming schemes.

It’s the same sort of activity as the 2017 ICO boom, and it’s still illegal securities & non-compliant activity.

The volume is significant enough now that regulators are likely going to crack down on this at some point soon. At the very least, they are going to enforce AML/KYC rules and the travel rule.

The big risk is that they are going to force non-compliant US-linked dexes (like Uniswap) to comply or shut down. The SEC took action against etherdelta in 2018, I don’t see any reason why they won’t do the same for projects like Uniswap.

The money printing elites at Wall St & the Central Banks are not going to just bend over and hand the keys to the money printer over to silicon valley VCs & smart contract developers.

This is the way I see it going:

Crypto is in a bubble like previous cycles.

The bubble is going to crash just like the last cycles.

ETH is going to eventually get rekt in BTC terms, and BTC is going to decouple from “Crypto” and continue the march towards a $10 Trillion global reserve asset.

ETH is already losing mindshare & developers to projects like Binance Smart Chain which are not pretending to be as decentralized as Bitcoin is. Future Ethereum-killers like Solana are being designed in a way that will siphon away even more of Ethereum’s network effects.

Users of DeFi & DEXes on BSC is now about ~10X the active users of DeFi on Ethereum.

Not only are Ethereum Maximalists & Network Effect Maximalists like Raoul Pal floating the idea of “the flippening” again amongst crypto & macro investors again … but now they are using Bitcoiner logic and saying that the flippening will happen even if Ethereum doesn’t scale.

This is a sign of euphoria. The same flippening conversations were being repeated near the top of the ETH price in 2017/2018.

Scaling.

Ethereum does have some scaling cards up it’s sleeve with ZK snarks, optimistic rollups & the eventual switch to PoS & ETH 2.0 … but that is a terrible design compared to the newer solutions like Solana which have the backing of crypto powerhouse FTX/Alameda Research.

All of these competing second layer & base layer scaling projects in the Ethereum ecosystem hurt the composability of Ethereum, and half of them have their own tokens which cannibalize the investor base.

After the DAO hack, Ethereum’s leadership has tried to intervene less and less to appear decentralized. However, with all these continual interventions, design changes and monetary policy changes, it’s continually showing that the claims of Ethereum’s decentralization have been greatly exaggerated.

What Ethereum does have on the network effects side is massive pools of silicon valley VC money, crypto fund money and the huge developer community.

However:

- The fee crisis has caused developers to start seeking other solutions like BSC, and there’s a huge exodus of keystone dapps & teams that were once Ethereum Maximalists to integrate with other chains, weakening the network effects of the moat of the smart contract development mindshare monopoly that ETH once had.

- The greed factor of the VCs backing Ethereum & defi is a double edged sword. They will always seek unicorn returns, which is why they start backing Ethereum killers & Ethereum competitors. Case in point, Solana & Flow. Cryptokitties broke Ethereum, so they developed their own blockchain for NFTs like NBA topshots which has more users now off-Ethereum. Hurts the network effects of the smart contract investor mindshare monopoly that ETH once enjoyed.

- Crypto Funds & Crypto Traders go where the yield is. Because Binance is 5–10X bigger than Coinbase, significant amount of capital is going over to other blockchains that are providing a better user experience and higher yields for their DeFi token-milking needs. Most funds & traders which used to be Ethereum maxis are now all over the place seeking yield anywhere they can get it.

I’ve seen a lot of Ethereum twitter influencers rationalize the fee crisis by saying things like “We will go over to BSC and capture the yield and then come back and invest it into ethereum” … a great coping mechanism perhaps, but by the “network effect” logic, they are actually contributing to the network effects of the competing blockchains.

Ethereum is definitely losing the Lindy lead for smart contract developers & for the DeFi & NFT use cases.

Back to the biggest risks of ETH & the DeFi coins.

The SEC, CFTC, FinCen, Treasury, NYAG & DOJ are not just going to let this go without a fight — and unlike Bitcoin, the very public teams building DeFi projects & issuing their own moneys & unregistered securities can be hauled into court or congress.

Ethereum itself is still much more centralized than they like to claim.

Vitalik still has outsized influence over Ethereum, he proposed EIP 1559 & is using his influence making the silicon valley podcast rounds to push it through.

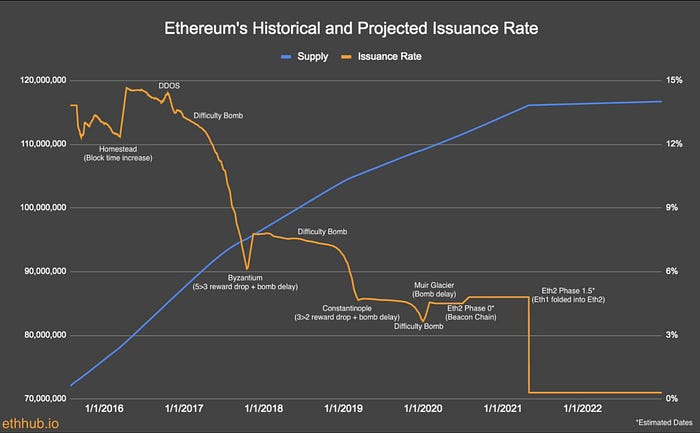

EIP 1559 is a significant change to Ethereum’s monetary policy. Every time they change the monetary policy, the long term credibility clock resets. Ethereum is starting at zero again this summer.

The 4–5 man team who maintain GETH pretty much have the yes/no over gas limit increases. 4 months ago they said no, this month they said yes.

Consensys still controls & funds a significant majority of infrastructure including Infura, Gitcoin & has a massive bag of ETH which will give them even more control after the switch to PoS.

DeFi teams are completely centralized.

Uniswap V3 is coming out soon with a commercial license …

Most of the DeFi teams are public, and governance votes are just simulated decentralization as the stake is controlled by a few participants & governance votes are just LARPs.

If you look at any DeFi coin’s distribution, you can see that these things look a lot more like equity cap tables than decentralized cryptocurrencies.

The claim of being a DAO is not going to fool the regulators or the courts.

Wyoming recently passed a DAO law, but it has a major caveat that if you are doing anything in violation of the existing federal or state laws, your DAO status can be revoked … this pretty much invalidates 90% of existing DAOs which are just centralized teams with VC backers printing themselves a premine & claiming decentralization.

These things all fail the Howey Test & are in violation of AML/KYC/FATF rules.

So while crypto folks like to say that Uniswap is unstoppable, I think it’s pretty easy to stop. Whether or not governments choose to stop it is what you’re betting on by buying ETH & DeFi coins.

I just don’t believe that Wall St & Central Banks will allow silicon valley unicorn smart contract devs & quants to usurp control of financial system without a fight.

Since it’s not actually decentralized, they will win the fight against DeFi.

They are rebuilding everything that’s wrong with Wall St on a blockchain, including the insider elites that control it all.

Bitcoin is actually the most decentralized cryptocurrency, so they will lose the fight against Bitcoin.